What is the Section 179 deduction?

Section 179 allows businesses to deduct the full purchase price of qualifying equipment and software in the year it is placed in service, rather than depreciating it over several years. For 2026, the deduction limit is \(2,560,000, with a phase-out threshold of \)4,090,000 in total equipment purchases, following the permanent increase enacted by the One Big Beautiful Bill Act (OBBBA) in July 2025.

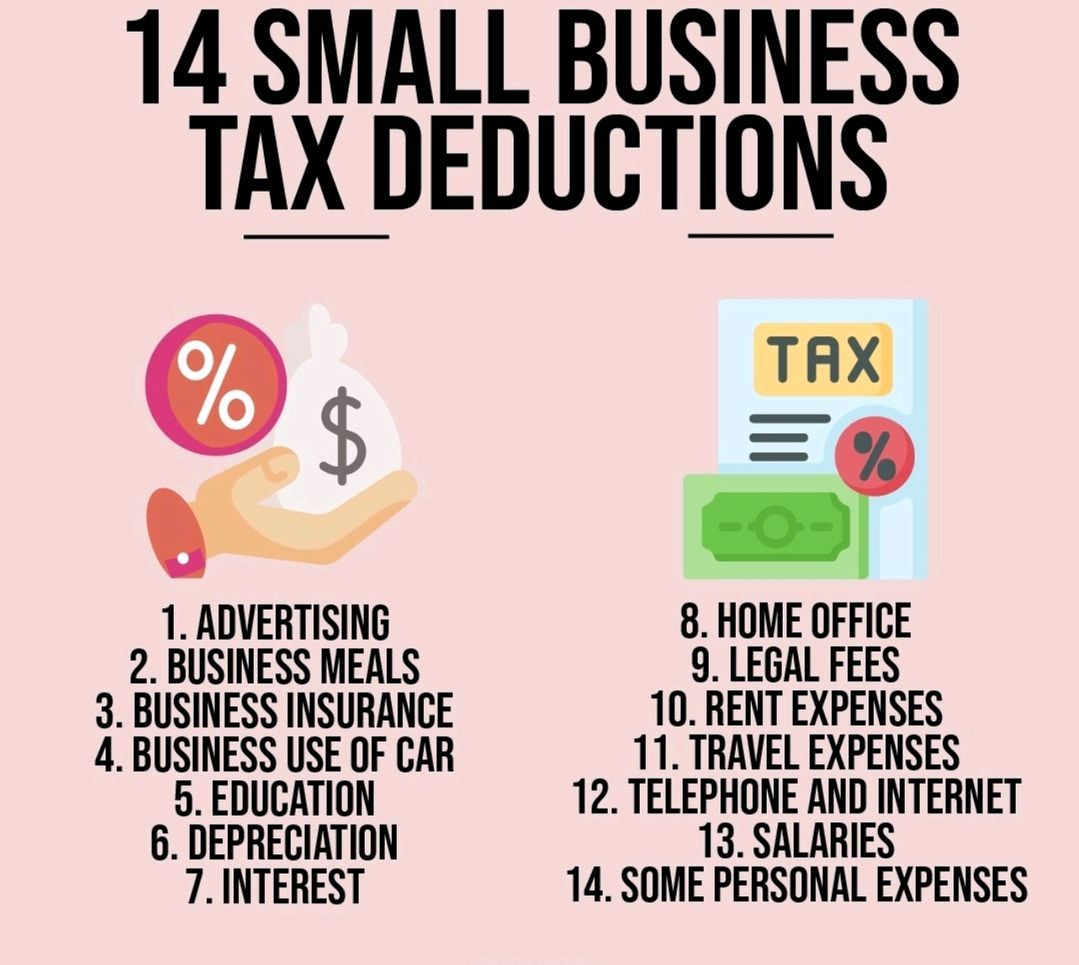

Tax deductions are one of the most powerful tools available to small business owners in the United States. Every legitimate business expense that qualifies as a deduction directly reduces your taxable income, and the cumulative effect of properly tracking and claiming all available deductions can save thousands or even tens of thousands of dollars per year. Despite this, studies consistently show that small business owners miss significant deductions simply because they are unaware of what qualifies or fail to maintain adequate records.

This guide provides a comprehensive overview of every major tax deduction available to US small businesses in 2026. It covers Section 179 expensing, bonus depreciation, the home office deduction, vehicle expenses, health insurance deductions, the Qualified Business Income (QBI) deduction, startup cost deductions, retirement plan contributions, and dozens of commonly overlooked deductions that can add up to substantial savings.

Section 179 Expensing

Section 179 of the Internal Revenue Code allows businesses to deduct the full purchase price of qualifying equipment and software purchased or financed during the tax year, rather than depreciating it over several years. This immediate expensing provision is one of the most valuable deductions for businesses that purchase equipment.

2026 Limits (Post-OBBBA, Adjusted Annually for Inflation)

| Parameter | Amount |

|---|---|

| Maximum deduction | $2,560,000 |

| Phase-out threshold | $4,090,000 |

| Maximum vehicle deduction (SUV > 6,000 lbs) | $32,000 |

| Maximum vehicle deduction (passenger vehicle) | ~$20,400 (first year) |

Qualifying Property

- Machinery and equipment

- Computers, laptops, tablets, and peripherals

- Office furniture and fixtures

- Off-the-shelf software

- Certain improvements to nonresidential real property (roofs, HVAC, fire protection, security)

- Vehicles used for business (with limitations)

- Certain listed property used more than 50% for business

Non-Qualifying Property

- Real property (buildings, land)

- Property used outside the US

- Property acquired from related parties

- Property used 50% or less for business purposes

- Inventory or property held for sale

Section 179 is particularly valuable for businesses that need to make large equipment purchases. Instead of depreciating a \(100,000 piece of equipment over 5 to 7 years, you can deduct the full amount in the year of purchase, reducing your taxable income by \)100,000 immediately. For a business in the 24% tax bracket, this saves $24,000 in taxes in the current year. However, the equipment must be placed in service (actually used for business) during the tax year to qualify - simply purchasing it is not sufficient.

Bonus Depreciation

Bonus depreciation allows businesses to deduct a percentage of the cost of qualifying assets in the first year they are placed in service, in addition to regular depreciation. The Tax Cuts and Jobs Act originally set bonus depreciation at 100% for assets placed in service from 2018 through 2022, after which it began phasing down toward 0% by 2027. The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, permanently restored 100% bonus depreciation for qualifying property acquired and placed in service on or after January 19, 2025:

| Tax Year | Bonus Depreciation Rate |

|---|---|

| 2018-2022 | 100% |

| 2023 | 80% |

| 2024 | 60% |

| Jan 1-18, 2025 | 40% (transitional, pre-OBBBA) |

| Jan 19, 2025 onward | 100% (restored permanently by OBBBA) |

| 2026 and beyond | 100% (permanent, no further phase-down) |

Bonus depreciation applies to new and used property with a recovery period of 20 years or less. Unlike Section 179, there is no dollar limit on bonus depreciation and it can create a net operating loss.

Home Office Deduction

If you use a portion of your home regularly and exclusively for business, you can deduct home office expenses using one of two methods.

Simplified Method

- $5 per square foot of home office space

- Maximum 300 square feet

- Maximum deduction: $1,500

- No depreciation calculations required

- Cannot carry forward unused deductions

Regular Method

The regular method requires calculating the actual expenses of maintaining your home and applying the business-use percentage:

| Expense Category | Deductible? | Calculation |

|---|---|---|

| Mortgage interest or rent | Yes | Business % of total |

| Property taxes | Yes | Business % of total |

| Homeowners/renters insurance | Yes | Business % of total |

| Utilities (electric, gas, water) | Yes | Business % of total |

| Internet service | Yes | Business % of total |

| Home repairs (general) | Yes | Business % of total |

| Home repairs (office only) | Yes | 100% |

| Depreciation of home | Yes | Business % of depreciable basis |

The business-use percentage is calculated by dividing the square footage of your office by the total square footage of your home. A 200-square-foot office in a 2,000-square-foot home represents a 10% business use.

The home office deduction is frequently audited, so maintaining proper documentation is essential. The space must be used “regularly and exclusively” for business - a guest bedroom that doubles as an occasional office does not qualify. Take photos of your dedicated workspace, keep measurements, and maintain records of all home expenses. For business owners whose actual expenses significantly exceed $1,500, the regular method can provide substantially larger deductions, especially for those with high rent or mortgage payments.

Vehicle Expenses

Business owners who use a vehicle for business purposes can deduct vehicle expenses using one of two methods.

Standard Mileage Rate

For 2026, the IRS standard mileage rate is expected to be approximately 67 to 70 cents per mile (adjusted annually). This rate covers gas, insurance, maintenance, depreciation, and all operating costs. You simply multiply business miles driven by the rate.

Actual Expense Method

Under the actual expense method, you deduct the business-use percentage of all actual vehicle expenses:

- Gas and oil

- Insurance premiums

- Repairs and maintenance

- Tires

- Registration and license fees

- Depreciation or lease payments

- Parking and tolls (deductible under either method)

| Method | Best For | Record-Keeping |

|---|---|---|

| Standard Mileage | Lower-cost vehicles, high mileage | Mileage log required |

| Actual Expense | Expensive vehicles, lower mileage | Detailed expense records + mileage log |

Regardless of which method you choose, you must maintain a contemporaneous mileage log that records the date, destination, business purpose, and miles driven for each trip.

Heavy Vehicle Exception

Vehicles with a gross vehicle weight rating (GVWR) over 6,000 pounds qualify for enhanced deductions. These vehicles (including many SUVs, trucks, and vans) can be fully expensed under Section 179 up to the annual limit (approximately $28,900 for SUVs in 2026, no limit for trucks and vans over 6,000 lbs). This provision has made vehicles like the Ford F-150, Chevrolet Suburban, and BMW X7 popular business vehicle choices.

Health Insurance Deduction

Self-employed individuals (including sole proprietors, LLC members, and S-Corp shareholders who own more than 2% of the company) can deduct 100% of health insurance premiums paid for themselves, their spouse, and their dependents. This deduction is taken on the personal tax return as an adjustment to income (not on Schedule C), meaning it reduces adjusted gross income even if you do not itemize deductions.

To qualify:

- You must not be eligible for employer-sponsored health insurance through another job (or a spouse’s job)

- The insurance plan must be established under the business

- S-Corp shareholders must have premiums paid by the corporation and reported as W-2 income

This deduction covers medical, dental, and vision insurance premiums, as well as qualified long-term care insurance premiums (subject to age-based limits).

Qualified Business Income (QBI) Deduction

The QBI deduction (Section 199A) allows eligible taxpayers with pass-through business income to deduct up to 20% of their qualified business income. This effectively reduces the top marginal rate on pass-through income from 37% to 29.6%.

Eligibility

| Business Type | Eligible? | Limitations |

|---|---|---|

| Sole proprietorship | Yes | Income thresholds for specified service businesses |

| LLC (taxed as partnership) | Yes | Income thresholds for specified service businesses |

| S-Corporation | Yes | Income thresholds for specified service businesses |

| C-Corporation | No | N/A |

Income Thresholds (2026 Estimates)

- Below \(201,750 (single) / \)403,500 (married filing jointly): Full 20% deduction available regardless of business type (2026 figures per IRS Rev. Proc. 2025-32)

- Above threshold, fully phased out at \(276,750 (single) / \)553,500 (married filing jointly): Deduction may be limited or eliminated for Specified Service Trades or Businesses (SSTBs)

- SSTBs include: Health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage, and any business where the principal asset is the reputation or skill of employees or owners

The QBI deduction is one of the most valuable tax benefits for pass-through business owners, but it has complex rules that trip up many taxpayers. If your business is an SSTB and your taxable income is above the threshold, you may lose part or all of the deduction. However, even within the SSTB category, strategic tax planning can help - for example, splitting a business into SSTB and non-SSTB components, maximizing W-2 wages (for the W-2/UBIA limitation), or managing taxable income to stay below the threshold through retirement contributions and other deductions.

Startup Cost Deduction

The IRS allows you to deduct up to \(5,000 in startup costs and \)5,000 in organizational costs in your first year of business. If total startup costs exceed \(50,000, the \)5,000 deduction begins to phase out dollar-for-dollar. Remaining startup costs must be amortized over 180 months (15 years).

Qualifying Startup Costs

- Market research and analysis

- Pre-opening advertising and marketing

- Employee training before the business opens

- Travel to establish the business (scouting locations, meeting suppliers)

- Consultant fees for business planning

- Costs of investigating the creation or acquisition of the business

Qualifying Organizational Costs

- State filing fees (articles of organization/incorporation)

- Legal fees for preparing operating agreements, bylaws, or partnership agreements

- Accounting fees for setting up the business structure

- Costs of organizational meetings

Retirement Plan Contributions

Small business retirement plans offer dual benefits: they reduce current-year taxable income and build tax-deferred retirement savings. The contribution limits vary by plan type.

| Plan Type | Employee Contribution Limit (2026 est.) | Employer Contribution | Total Maximum | Best For |

|---|---|---|---|---|

| SEP-IRA | N/A (employer-only plan) | Up to 25% of compensation | ~$69,000 | Self-employed, no employees |

| Solo 401(k) | ~\(23,500 + \)7,500 catch-up (50+) | Up to 25% of compensation | ~$69,000 | Self-employed, no employees |

| SIMPLE IRA | ~\(16,500 + \)3,500 catch-up (50+) | 2% of comp or 3% match | ~$16,500 employee + match | Small businesses with employees |

| Traditional 401(k) | ~\(23,500 + \)7,500 catch-up (50+) | Discretionary | ~$69,000 total | Businesses with employees |

For self-employed individuals and S-Corp owner-employees, the Solo 401(k) typically allows the highest total contribution due to the combination of employee and employer contributions.

Commonly Overlooked Deductions

Many legitimate business deductions are missed simply because business owners do not realize they qualify:

Professional development: Courses, certifications, conferences, and books related to your current business are deductible. This includes online courses, industry conferences (including travel), and professional certifications.

Business insurance: All insurance premiums for business-related policies are deductible, including general liability, professional liability (E&O), cyber liability, commercial property, and business interruption insurance.

Software and subscriptions: Business software subscriptions (accounting, design, project management, CRM), industry publications, and professional association memberships are deductible.

Bank and credit card fees: Monthly bank service charges, merchant processing fees, wire transfer fees, and annual credit card fees for business credit cards are all deductible.

Legal and professional fees: Attorney fees, accounting fees, consulting fees, and other professional services related to your business are deductible.

Bad debts: If you use the accrual method of accounting and a customer does not pay, you can deduct the unpaid amount as a bad debt expense.

Meals: Business meals (meals with clients, prospects, or business associates where business is discussed) are 50% deductible. The meal must have a clear business purpose and cannot be lavish or extravagant. Meals provided to employees for the convenience of the employer may be subject to different rules.

Moving expenses for business equipment: The cost of moving business equipment, inventory, or office furnishings from one business location to another is fully deductible.

Charitable contributions: C-Corporations can deduct charitable contributions up to 10% of pre-deduction taxable income. Pass-through entities pass charitable deductions through to individual owners.

Record-Keeping Requirements

The IRS requires businesses to maintain records that support all income and deductions claimed. For most deductions, you should keep:

- Receipts or invoices for all expenditures over $75

- Bank and credit card statements

- Mileage logs (contemporaneous records)

- Records of business purpose for travel, meals, and entertainment expenses

- Depreciation schedules for capital assets

- Employment tax records for at least 4 years

| Record Type | Retention Period |

|---|---|

| Tax returns and supporting documents | 7 years |

| Employment tax records | 4 years after tax is due or paid |

| Business asset records | Duration of ownership + 7 years |

| General business records | 7 years |

| Records supporting loss deduction | 7 years |

Good record-keeping software (QuickBooks, Xero, FreshBooks) can automate much of the documentation process and make tax preparation significantly easier and less expensive.

For information on how these deductions interact with your overall tax obligations, see our corporate tax guide. For information on choosing the right entity structure to optimize your tax position, see our guide to LLC vs C-Corp vs S-Corp. Small business owners looking for additional funding to support their growth should review our guide to SBA loans and grants.

Entrepreneurs comparing US tax deductions with those available in other countries should review our tax guides for the United Kingdom and Singapore, which offer their own unique tax optimization strategies.

Section 179 and Bonus Depreciation 2026 Limits

Section 179 and bonus depreciation limits are worth tracking closely because equipment expensing rules have shifted materially under TCJA and subsequent revisions.

| Provision | 2026 Limit | Notes |

|---|---|---|

| Section 179 expensing maximum | $2,560,000 | Made permanent and roughly doubled by OBBBA (July 2025); indexed annually for inflation |

| Section 179 phase-out threshold | $4,090,000 | Dollar-for-dollar reduction above this purchase level |

| Bonus depreciation rate | 100% (permanent) | Restored permanently by OBBBA for property acquired and placed in service on or after January 19, 2025 |

| Qualifying property | Tangible personal property, off-the-shelf software, qualified improvement property | Section 168(k) |

| Passenger auto Section 280F limits | \(20,400 first year (with bonus) / \)12,400 (without) | Subject to annual updates |

| SUV cap (over 6,000 lbs GVW) | $32,000 Section 179 | Heavy vehicle loophole |

Qualified Business Income (QBI) Section 199A

The 20% QBI deduction is one of the most valuable deductions for pass-through entities. QBI calculations should be run for every LLC, partnership, and S-Corp.

| Feature | Detail |

|---|---|

| Base deduction | 20% of qualified business income from pass-through businesses |

| Taxable income threshold (single, 2026) | \(252,150 begins phase-in; \)305,650 fully phased (Specified Service Trades or Businesses) |

| Taxable income threshold (joint, 2026) | \(504,300 begins; \)611,300 fully phased |

| SSTBs excluded at full phase-in | Health, law, accounting, actuarial, performing arts, consulting, athletics, financial services, investing, any business where principal asset is reputation/skill |

| Wage/UBIA limits above threshold | Greater of 50% of W-2 wages, or 25% of W-2 wages + 2.5% of unadjusted basis immediately after acquisition (UBIA) of qualified property |

| Permanence | Made permanent by the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, removing the previous scheduled sunset on 31 December 2025. The 20% rate is unchanged; the phase-in range was widened and a \(400 minimum deduction was added for taxpayers with at least \)1,000 of active QBI, effective for tax years beginning after 2025 |

According to the Internal Revenue Service Publication 535 and Section 199A of the Internal Revenue Code, the Qualified Business Income deduction allows eligible taxpayers to deduct up to 20% of their qualified business income from a qualified trade or business plus 20% of qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income - subject to W-2 wage and unadjusted basis limitations that apply above certain taxable income thresholds [5].

Home Office Deduction Methods

| Method | Formula | Advantages | Disadvantages |

|---|---|---|---|

| Simplified method | \(5 per square foot, up to 300 sq ft, max \)1,500 | No depreciation recapture on sale; minimal recordkeeping | Cap limits deduction for larger offices |

| Regular method | Business % of home expenses (utilities, mortgage interest, property tax, depreciation, insurance) | Potentially larger deduction | Depreciation recapture on sale; detailed records required |

| Requirements | Exclusive and regular use; principal place of business OR meeting clients; separate structure used in trade/business | - | - |

Meals and Entertainment Post-TCJA

The TCJA substantially restricted meals and entertainment deductions. The current rules break down as follows:

- Business meals: 50% deductible (temporary 100% for restaurant meals expired after 2022)

- Entertainment: Not deductible (e.g., sporting events, concerts, country club dues)

- Employee meals at employer premises: 50% through 2025, 0% thereafter (absent Congressional action)

- De minimis meals (holiday parties, occasional snacks): 100% deductible

- Travel meals: 50% deductible; per diem rates from IRS Publication 1542 acceptable

Common Small Business Tax Mistakes

- Mixing personal and business expenses: Most common cause of audit adjustments; disallowed on audit even if substantively business-related.

- Inadequate documentation for vehicle use: Missing mileage logs invalidate vehicle deductions even if the business use was legitimate.

- Not tracking home office square footage: Arbitrary estimates trigger examinations.

- Missing 1099 issuance: Payments of \(600+ to non-corporate contractors require Form 1099-NEC; failure carries \)310+ per-form penalty.

- Failing to make Section 83(b) election: For founders receiving restricted stock, failing to file within 30 days forfeits the ability to treat vesting as current income at low FMV.

Related Corpy Resources

- United States business guide for a full overview of doing business in United States

- Corporate tax in United States for related articles on this topic

- Company formation in United States to explore adjacent considerations

- Business laws in United States to explore adjacent considerations

- Free zones in United States to explore adjacent considerations

References

- Internal Revenue Service (IRS). https://www.irs.gov/

- IRS Publication 542 - Corporations. https://www.irs.gov/publications/p542

- US Department of the Treasury. https://home.treasury.gov/

- OECD Inclusive Framework on BEPS. https://www.oecd.org/tax/beps/

- World Bank Doing Business Archive. https://archive.doingbusiness.org/

- IRS Publication 535, Business Expenses. https://www.irs.gov/publications/p535

- Internal Revenue Code Section 199A, Qualified Business Income Deduction. https://www.law.cornell.edu/uscode/text/26/199A

Frequently Asked Questions

What is the Section 179 deduction?

Section 179 allows businesses to deduct the full purchase price of qualifying equipment and software in the year it is placed in service, rather than depreciating it over several years. For 2026, the deduction limit is \(2,560,000, with a phase-out threshold of \)4,090,000 in total equipment purchases, following the permanent increase enacted by the One Big Beautiful Bill Act (OBBBA) in July 2025. Qualifying items include computers, office furniture, machinery, vehicles (with limits), and off-the-shelf software.

What is the QBI deduction?

The Qualified Business Income (QBI) deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income from pass-through entities (sole proprietorships, partnerships, S-Corps, and LLCs). There are income limitations and restrictions for specified service trades or businesses (such as law, accounting, and consulting) above certain income thresholds.

Can I deduct home office expenses?

Yes, if you use a portion of your home regularly and exclusively for business. You can use the simplified method (\(5 per square foot, up to 300 square feet, maximum \)1,500) or the regular method (calculating actual expenses based on the percentage of your home used for business). The space must be your principal place of business or where you regularly meet clients.

Are startup costs deductible?

Yes. You can deduct up to \(5,000 in startup costs and \)5,000 in organizational costs in your first year of business. If your total startup costs exceed \(50,000, the \)5,000 deduction begins to phase out. Remaining startup costs must be amortized over 15 years (180 months). Qualifying startup costs include market research, advertising before opening, employee training, and travel to establish the business.

How this guide was produced

Official sources

- Small Business and Self-Employed Tax Center - IRSIRS (U.S.)

- Internal Revenue Service (IRS)U.S. Government

Important: This guide describes United States law and is for general information only. It is not legal, tax or accounting advice. The US has federal and state rules: companies are formed under state law (Delaware is common) while federal tax is administered by the IRS and immigration by USCIS, so requirements differ by state and change over time. Verify any figure against the linked official source before you act on it.

Contributors

Need expert help?

Find a specialist

Browse accountants, lawyers and formation agents. Free to enquire, no account required.

Find a Specialist →