Why the UK Remains the Best Jurisdiction for Non-Resident Company Formation in 2026

Among all the jurisdictions covered in our company formation guides, the United Kingdom offers arguably the most cost-effective and credible route to a legitimate, internationally respected business entity. At GBP 12 for an online filing and a typical turnaround of under 24 hours, a UK Private Limited Company (Ltd) can be formed faster and for less money than registering a vehicle in most countries.

For non-residents, the appeal is compounded by what the UK does not require: no local director, no minimum share capital, no notarisation, no in-person visit, and no restriction on foreign ownership. Every aspect of the process can be completed remotely from anywhere in the world.

Post-Brexit, the UK is no longer part of the EU single market, but it remains one of the world's most respected legal jurisdictions. English contract law governs a significant share of global commercial agreements, UK companies are accepted by banks and payment processors worldwide, and the Companies House public register provides a level of institutional credibility that offshore structures often cannot match.

This guide walks through every step of forming and operating a UK Ltd as a non-resident in 2026, from choosing a company name through to annual compliance. For a broader comparison of how UK formation costs compare to other jurisdictions, see our country comparison tool.

Company Types Available in the UK

Before filing, it is important to choose the right structure. The UK offers several entity types, but the vast majority of non-resident founders should use a Private Limited Company (Ltd).

Private Limited Company (Ltd)

The standard choice. Shareholders have limited liability (they cannot lose more than the value of their shares). The company is a separate legal person. It can open bank accounts, enter contracts, hold intellectual property, and employ people in its own name. Profits are subject to corporation tax, and dividends can be paid to shareholders.

Limited Liability Partnership (LLP)

An LLP is tax-transparent: profits are allocated to members and taxed at the member level, not the entity level. This can be advantageous for professional services firms (law, accounting, consulting) where all partners are individuals in lower-tax jurisdictions, or for structures where the partners are themselves companies in favourable jurisdictions. However, LLPs are more complex to administer and less familiar to non-UK counterparties than a standard Ltd.

Sole Trader

Not a separate legal entity. The individual and the business are the same person legally. Unlimited personal liability. Not appropriate for most non-residents building a scalable business.

| Structure | Limited Liability | Tax Transparent | Min. Directors | Best For |

|---|---|---|---|---|

| Private Ltd (Ltd) | Yes | No | 1 | Most businesses, e-commerce, SaaS, consulting |

| LLP | Yes (members) | Yes | 2 designated members | Professional services, fund structures |

| Sole Trader | No | Yes | N/A | Very small, low-risk freelance work only |

Step-by-Step: Companies House Registration

Step 1: Choose and Check Your Company Name

Your company name must be unique. Check availability using the Companies House name availability tool at find-and-update.company-information.service.gov.uk. The name must end in "Limited" or "Ltd" (or Welsh equivalents if registering in Wales). It cannot be the same as, or too similar to, an existing company name on the register.

Certain words require additional approval or are restricted:

- Sensitive words: Bank, Royal, National, International, Insurance, Trust, Chamber of Commerce, University -- these require approval from the relevant regulatory body before they can be used

- Government associations: Any name that implies government endorsement or connection requires Home Office approval

- Misleading names: Companies House can reject names that are likely to mislead the public as to the nature of the business

It is also worth checking that your chosen name is available as a domain name and trademark before filing, as Companies House registration does not give you trademark rights.

Step 2: Prepare Your Documents and Information

Before filing, gather the following:

- Memorandum of Association: A statement that subscribers wish to form the company. For online filing, this is generated automatically.

- Articles of Association: The rules governing how the company is run. You can use the Model Articles (standard template provided by Companies House, suitable for most companies) or submit custom articles. Custom articles are needed for complex share structures, drag-along/tag-along rights, investor protections, or weighted voting.

- Director details: Full name, date of birth, nationality, country of residence, and a service address (a public address used for official correspondence -- this can be your virtual office address, protecting your residential address from public view). Residential address is also required but kept private at Companies House.

- Shareholder details: Name, address, and number of shares held. For a simple company, the director and shareholder can be the same person.

- Registered office address: A physical address in England and Wales (or Scotland if registering there, or Northern Ireland). This appears on the public register.

- SIC code: The Standard Industrial Classification code describing your business activity. You can find the correct code in the Companies House SIC list.

Step 3: File Online at Companies House

Go to www.gov.uk/limited-company-formation and choose to register online. You will need to create a Government Gateway account if you do not have one. The online form is called the IN01. Completing it typically takes 20-30 minutes for a straightforward company. The government fee is GBP 12, payable by debit or credit card online.

Companies House processes online applications during business hours. If you file before 3pm on a business day, you will typically receive your Certificate of Incorporation the same day. Applications filed after 3pm are usually processed the following morning.

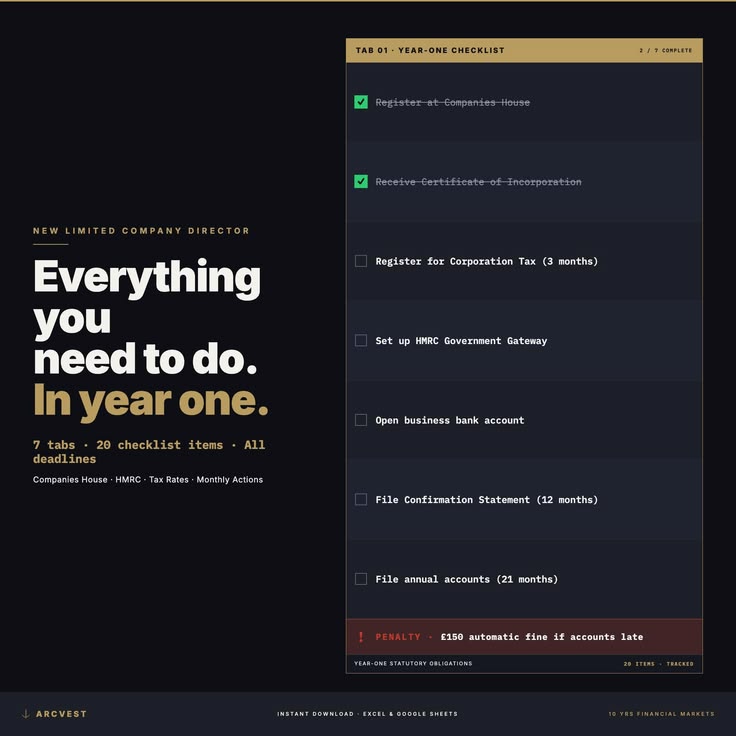

Step 4: Receive Your Certificate of Incorporation

Upon approval, Companies House issues a Certificate of Incorporation confirming your company's name, company number, and date of incorporation. This is a legally significant document. Keep a digital and physical copy. Your company number is a permanent identifier used in all dealings with HMRC, banks, and counterparties.

Step 5: Register for Corporation Tax with HMRC

Within three months of starting to trade (or receiving income), you must notify HMRC that your company is active and register for Corporation Tax. This is done at www.hmrc.gov.uk using your company's Unique Taxpayer Reference (UTR), which HMRC posts to your registered office address within approximately two weeks of incorporation.

You will also need to set up a Business Tax Account with HMRC, through which you will file all future tax returns online.

Step 6: Obtain a UK Business Address (if needed)

If you do not already have a UK address, you will need to arrange one before filing. See the section below on virtual office providers.

Step 7: Open a Business Bank Account

A UK company can legally operate without a dedicated business bank account, but in practice every company needs one. Options for non-residents are covered in detail in the banking section below.

UK Address Options for Non-Residents

A common misconception is that a UK Ltd company requires you to live in the UK. It does not. However, the company must have a registered office address that is a physical address in the UK (England/Wales, Scotland, or Northern Ireland depending on where you register). A PO box alone does not suffice.

Virtual office providers offer a compliant registered office address along with mail handling services. The most commonly used options include:

| Provider | Location | Registered Office Price | Extras |

|---|---|---|---|

| Hoxton Mix | London EC1 | From GBP 10/mo | Mail scanning, forwarding, meeting rooms |

| 1st Formations | London + regional | From GBP 39/yr | Director service address, mail forwarding |

| Your Company Formations | London | From GBP 29/yr | Registered office + director service address bundle |

| Regus | UK-wide (50+ locations) | From GBP 150/mo | Premium addresses, access to meeting rooms |

| Be Offices | London + regional | From GBP 30/mo | Physical coworking access available |

Your director service address (the public address used for correspondence with you as a director) can be different from the company's registered office. Most virtual office providers offer both as a bundle. This is important for privacy: if you use a virtual office service address, your home address is kept private on the public register.

UK Business Bank Accounts for Non-Residents

Opening a bank account is often the hardest part of the process for non-residents. Traditional UK high street banks have historically required an in-person visit, proof of UK address, and extensive due diligence documentation, making them effectively inaccessible to most non-residents remotely.

The UK fintech sector has largely solved this problem. The following options are used by non-resident UK Ltd companies:

| Bank | Non-Resident Friendly | Monthly Fee | Key Features | Limitations |

|---|---|---|---|---|

| Tide | Yes (most accessible) | From GBP 1/mo | Instant online application, invoicing, expense cards | No cash deposits, some MCC restrictions |

| Starling Business | Partially (UK address helps) | Free | Full-featured, FSCS-protected, good integrations | Application may require UK address verification |

| Monzo Business | Difficult | Free / GBP 5/mo Pro | Strong app, FSCS-protected | Generally requires UK address and phone number |

| Revolut Business | Yes | From GBP 0/mo | Multi-currency, crypto, global transfers | Not FSCS-protected, account closures can occur |

| Wise Business | Yes | GBP 45 setup + low fees | GBP sort code + account number, 40+ currencies | Not technically a bank, no overdraft/credit |

Tide is typically the most straightforward option for non-residents forming a new UK Ltd company. The application is entirely online, requires your Certificate of Incorporation, passport, and proof of home address, and accounts are usually approved within 24-48 hours. Wise Business is a strong complement or alternative, providing a genuine GBP sort code and account number that most payment processors and counterparties treat as a full UK bank account.

Traditional Banks (For Later Stage)

Barclays, HSBC, Lloyds, and NatWest remain the most trusted counterparties for enterprise clients and government contracts. Many large UK corporate clients prefer suppliers to hold accounts with high-street banks. These become more accessible once your company has trading history, UK clients, and ideally a UK-resident accountant acting as an introducer. At the time of formation, they are generally impractical for non-residents.

Corporation Tax in 2026

UK corporation tax applies to the profits of UK-resident companies (those incorporated in the UK or managed and controlled from the UK). The rates for 2026 are unchanged from the 2023 reform:

- Small profits rate: 19% on profits up to GBP 50,000

- Main rate: 25% on profits above GBP 250,000

- Marginal relief: For profits between GBP 50,000 and GBP 250,000, an effective rate that rises from 19% to 25% through marginal relief calculations

These thresholds are divided among associated companies (companies under common control), so if you own multiple UK companies, the thresholds apply to the group.

Filing the Company Tax Return (CT600)

The Company Tax Return (form CT600) must be filed online with HMRC every year, within 12 months of the end of the company's accounting period. The accounting period is typically 12 months and usually aligns with your company's financial year.

Crucially, corporation tax is due for payment 9 months and 1 day after the end of the accounting period -- three months before the filing deadline. Missing the payment deadline incurs interest. Missing the filing deadline incurs penalties starting at GBP 100 for one day late, rising significantly for extended delays.

Most non-resident owners use a UK-based accountant or accounting software such as FreeAgent, Xero, or QuickBooks to prepare and file the CT600. For details on allowable deductions and planning opportunities, see our UK corporate tax guide.

R&D Tax Credits

The UK offers one of the world's most generous research and development (R&D) tax relief schemes. For small and medium-sized enterprises (under 500 employees, under EUR 100 million turnover, under EUR 86 million balance sheet), the SME R&D scheme provides an additional 86% deduction on qualifying R&D expenditure (so GBP 100 of R&D spending becomes a GBP 186 deduction), plus a payable tax credit of 10% of losses surrendered for R&D purposes if the company is loss-making. Qualifying activities include software development, product development, and process improvement where technical uncertainty must be resolved. Many tech startups and product companies leave significant money unclaimed by not filing R&D claims.

VAT Registration

Value Added Tax (VAT) is a consumption tax charged at 20% on most goods and services in the UK. Registration is mandatory when your taxable turnover exceeds GBP 90,000 in any rolling 12-month period. Below this threshold, registration is voluntary but often commercially advantageous for B2B businesses whose clients are themselves VAT-registered (as they can reclaim the VAT you charge).

Making Tax Digital (MTD) for VAT

All VAT-registered businesses must comply with Making Tax Digital for VAT, which requires keeping digital VAT records using MTD-compatible software and submitting VAT returns directly from that software to HMRC (no manual entry via HMRC portal). Compatible software includes Xero, QuickBooks, Sage, and FreeAgent. VAT returns are submitted quarterly. VAT payment is due one month and seven days after the end of the quarter.

Post-Brexit VAT for International Sales

For e-commerce sellers, post-Brexit rules have significant implications. Selling goods to EU consumers requires charging import VAT in the destination EU country. For consignments under EUR 150, UK sellers can register for the EU IOSS (Import One Stop Shop) scheme to simplify VAT collection and remittance. Selling digital services to EU consumers requires either registering for VAT in each EU member state or using the EU's One Stop Shop (OSS) scheme by registering in one EU country.

Annual Confirmation Statement

The Annual Confirmation Statement must be filed with Companies House every 12 months from the date of incorporation. It confirms that the information Companies House holds about your company is accurate: officers, shareholders, registered office, and Standard Industrial Classification (SIC) code. The government fee is GBP 34 for online filing. Failure to file results in Companies House initiating a compulsory strike-off of the company.

Annual Accounts

UK companies must file annual accounts with both Companies House (public filing) and HMRC (as part of the corporation tax return).

- Micro-companies (turnover under GBP 632,000, balance sheet assets under GBP 316,000, fewer than 10 employees): May file abbreviated accounts at Companies House, protecting financial privacy.

- Small companies (turnover under GBP 10.2 million, assets under GBP 5.1 million, under 50 employees): May file abbreviated accounts without the strategic report or directors' report.

- Larger companies: Must file full accounts.

Deadline with Companies House: 9 months after the accounting period end date (for the first period, it is 21 months from the date of incorporation). Deadline with HMRC: 12 months after the accounting period end.

Persons with Significant Control (PSC) Register

UK companies must maintain a register of Persons with Significant Control -- any individual that holds more than 25% of shares, holds more than 25% of voting rights, holds the right to appoint or remove a majority of directors, or otherwise exercises significant influence or control. PSC information is reported to Companies House and is publicly accessible. Failure to maintain and file accurate PSC information is a criminal offence.

PAYE: Employing People Including Yourself

If your company pays a salary to anyone, including you as a director, it must register as an employer with HMRC and operate Pay As You Earn (PAYE). This involves registering as an employer, running payroll software, submitting Real Time Information (RTI) reports to HMRC each time employees are paid, deducting income tax and employee National Insurance Contributions (NICs) from salaries, and paying employer NICs (13.8% on earnings above the Secondary Threshold).

Many director-shareholders of small UK companies choose to take a low salary (around the Primary Threshold, approximately GBP 12,570 per year) and extract additional profit as dividends, which are taxed at lower rates than salary and do not attract NICs.

Post-Brexit Considerations for Non-EU Businesses

The UK's departure from the European Union has implications for UK Ltd companies with European operations or clients. The UK is no longer in the EU single market, so goods shipped between the UK and EU are subject to customs declarations and potentially import duties. UK financial services firms no longer have automatic EU passporting rights, and a separate EU entity is needed for EU financial services activities. The UK has its own UK GDPR framework, broadly equivalent to EU GDPR.

Despite these changes, a UK Ltd company remains highly credible and commercially effective for businesses serving global markets. For a direct comparison with EU jurisdictions, see our country comparison or review the corporate tax guide.

Full Cost Breakdown: Year 1 and Year 2+

| Cost Item | Year 1 (GBP) | Year 2+ (GBP/yr) | Notes |

|---|---|---|---|

| Companies House registration fee | 12 | 0 | One-off |

| Virtual registered office address | 120 - 240 | 120 - 240 | GBP 10-20/mo; Hoxton Mix, 1st Formations etc. |

| Director service address | 0 - 60 | 0 - 60 | Often bundled with registered office |

| Annual Confirmation Statement | 34 | 34 | Online filing; due annually |

| Business bank account (neobank) | 12 - 60 | 12 - 60 | Tide from GBP 1/mo; Revolut free plan available |

| Accountant (basic compliance) | 500 - 1,500 | 500 - 1,500 | CT600 + annual accounts; varies by complexity |

| Accounting software | 120 - 360 | 120 - 360 | FreeAgent (free via Starling/NatWest) or Xero |

| VAT registration | 0 | 0 | Free; only if turnover exceeds GBP 90k threshold |

| Total (low estimate) | 798 | 786 | Solo director, micro-company, Tide account |

| Total (high estimate) | 2,266 | 2,254 | Premium address, full accountant, Xero |

Common Mistakes Non-Residents Make

- Using a personal address as the registered office: This puts your home address on the public Companies House register permanently. Use a virtual office address instead.

- Missing the Corporation Tax registration deadline: HMRC must be notified within 3 months of starting to trade. Missing this can result in penalties even before the first tax return is due.

- Treating the company as a personal account: All company income and expenses should flow through the company bank account. Mixing personal and company finances causes accounting problems and HMRC scrutiny.

- Not keeping minutes and resolutions: Keep records of key decisions including dividend declarations.

- Declaring dividends without retained profits: Dividends can only be paid from distributable reserves (post-tax profits). Paying dividends when the company has no distributable reserves is unlawful.

- Assuming the company is automatically dormant: If the company has a bank account, receives any income, or makes any payments, it is not dormant and must file accounts and a CT600 accordingly.

A UK Ltd company gives non-residents access to one of the world's most credible commercial jurisdictions at a fraction of the cost of comparable alternatives. The key to making it work is understanding the ongoing compliance requirements from day one, not as an afterthought.

Summary: Is a UK Ltd Right for You?

A UK Private Limited Company is the right choice if you need a credible, English-law entity accepted by global banks and payment processors, at the lowest possible setup cost. It works particularly well for SaaS and software companies serving global B2B clients, e-commerce businesses that want Stripe and PayPal without complication, consultants and agencies serving UK or international corporate clients, founders who want to raise investment (UK VC ecosystem and SEIS/EIS tax incentives for investors are significant advantages), and non-residents who want to hold UK intellectual property or assets under a respectable legal entity.

Where a UK Ltd may not be the best choice: if you need EU single market access for regulated financial services, or if the UK corporation tax rate (up to 25%) is significantly higher than alternatives you qualify for. In those cases, our country comparison tool and corporate tax guides can help identify the optimal structure. You can also use our document checklist to prepare everything you need before filing.

Frequently Asked Questions

Can a non-UK resident own a UK Ltd company?

Yes. There is no residency or nationality requirement to own or direct a UK Limited Company. Non-residents can be directors, shareholders, and persons with significant control. The only requirement is a registered office address in England and Wales, Scotland, or Northern Ireland, which can be provided by a virtual office service.

Do I need a UK address for a UK Ltd company?

Your company must have a registered office address in the UK. This must be a physical address (not a PO box) and is publicly listed at Companies House. Virtual office providers such as Hoxton Mix, Regus, and 1st Formations offer compliant registered office addresses from around GBP 10-20 per month. Your personal residential address does not need to be in the UK.

What is the UK corporation tax rate in 2026?

The UK corporation tax rate for 2026 is 19% on profits up to GBP 50,000 and 25% on profits above GBP 250,000. Companies with profits between GBP 50,000 and GBP 250,000 receive marginal relief, resulting in an effective rate that rises gradually between those thresholds.

How do I open a bank account for a UK Ltd as a foreigner?

Traditional UK high street banks (Barclays, HSBC, Lloyds) typically require an in-person visit and proof of UK address, making them very difficult for non-residents. The most practical options are neobanks: Tide is the most popular for non-resident UK Ltd companies and can be opened entirely online. Starling Business and Wise Business (which provides a GBP sort code and account number) are also widely used alternatives.

What is Making Tax Digital?

Making Tax Digital (MTD) is HMRC’s programme to digitalise the UK tax system. For VAT, all VAT-registered businesses must use MTD-compatible accounting software (such as Xero, QuickBooks, or FreeAgent) to keep digital records and submit VAT returns. MTD for Income Tax is scheduled for mandation from April 2026 for self-employed individuals and landlords with income above GBP 50,000.

Do I need a local director for a UK Ltd?

No. A UK Limited Company requires at least one director, but there is no requirement for that director to be a UK resident or citizen. A single non-resident individual can be the sole director and shareholder. The company must, however, have a UK registered office address. Some banks and payment processors may prefer or require a UK-resident director, which is a commercial consideration rather than a legal one.

How this guide was produced

Official sources

- Companies HouseUK Government

- HM Revenue & CustomsUK Government

Important: This guide describes law in the United Kingdom and is for general information only. It is not legal, tax or accounting advice. Companies are registered at Companies House and tax is administered by HMRC; Scotland and Northern Ireland have separate legal systems for some matters. Rates and thresholds change and depend on your circumstances. Verify any figure against the linked official source before you act on it.

Need expert help?

Find a specialist

Browse accountants, lawyers and formation agents. Free to enquire, no account required.

Find a Specialist →